Business Expenses the IRS May Disallow: Lessons for Business Owners

A recent Tax Court case shows how the IRS may disallow business deductions when personal expenses, family costs, travel, meals, reimbursements, and shareholder advances are run through a company without proper records or a clear business purpose. For business owners, the lesson is direct: keep clean records, separate personal and business spending, and document why each expense belongs to the business.

Tax Court Denies More Than $456,000 in Horse Business Losses: What Schumacher v. Commissioner Means for Hobby Loss Deductions

The Tax Court denied more than $456,000 in horse business losses after finding that weak financial records, commingled funds, no credible profit plan, and eighteen years of losses outweighed the taxpayers’ expertise and substantial effort. Schumacher v. Commissioner shows what business owners must document to protect deductions under Section 183.

A Missing Sentence Can Erase a Charitable Deduction: Lessons From Wells v. Commissioner

One missing sentence in a charity receipt can eliminate an otherwise valid tax deduction. Wells v. Commissioner shows why donors must obtain a timely acknowledgment that states whether the charity provided goods or services, and why Form 8283 is not enough.

Should Your Business Elect S Corporation Status? Tax Savings, Risks, and When It Makes Sense

Should your business elect S corporation status? Learn how reasonable compensation, Section 199A, accountable plans, shareholder basis, health insurance, state taxes, and distribution rules determine whether the election creates real savings.

Are Trust Distributions Taxable to Beneficiaries? Income, Principal, and Schedule K1 Rules

Received money or property from a trust? Learn when beneficiaries owe tax, when principal is generally nontaxable, and how Schedule K1 controls the reporting.

Selling Depreciated Business or Rental Property? How Depreciation Recapture Can Increase Your Tax Bill

Selling rental property or business assets can create unexpected taxes through depreciation recapture. Learn how Sections 1245 and 1250 affect your gain and why Section 1231 does not always produce capital gain treatment.

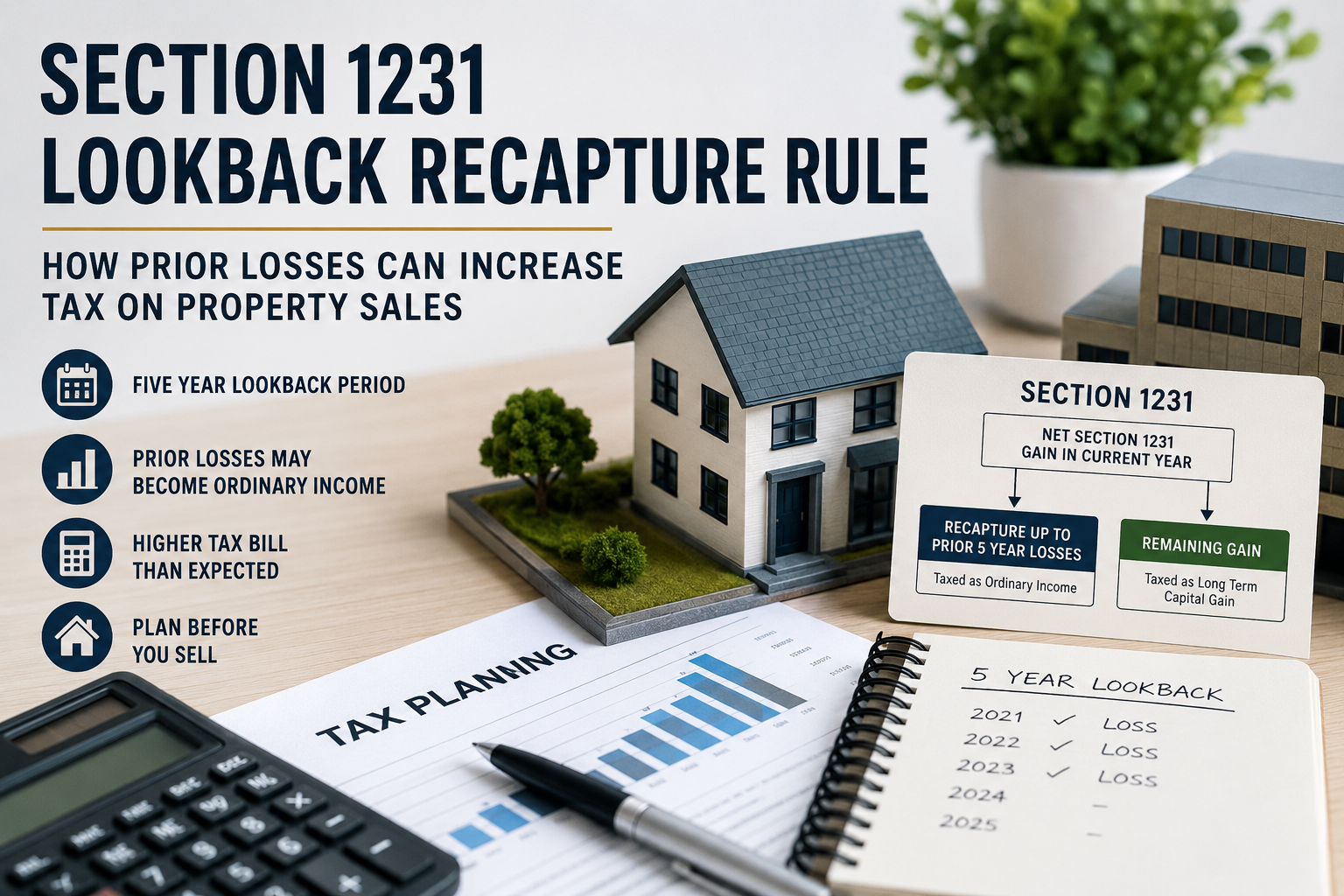

The Hidden Tax Trap in Section 1231: How the Five Year Lookback Rule Can Turn Capital Gains Into Ordinary Income

Section 1231 property often provides the best of both tax worlds: ordinary loss treatment and capital gain treatment. However, many taxpayers overlook the five year lookback recapture rule that can convert current gains into ordinary income. Learn how the rule works before selling business or rental property.

Schedule C or Form 1065? How Husband and Wife LLC Owners Should Choose

Should a husband and wife LLC file Schedule C or Form 1065? Learn how community property rules affect eligibility and compare the filing costs, self employment tax treatment, deadlines, and state requirements of each option.

Selling Business or Rental Property? Why Section 1231 Can Produce Better Tax Results Than Capital Gains

Selling rental property, commercial real estate, or business assets? Understanding Section 1231 before the sale closes can create significant tax savings and help you avoid costly tax surprises. Learn how gains, losses, depreciation recapture, and the five year lookback rule affect your tax bill.

Can Rental Income Cause Your S-Corp To Lose Its Tax Status?

Many business owners keep their building after selling the operating business. A recent IRS ruling explains how rental income can create unexpected risks for certain S corporations and what business owners should consider before making a major business transition.

Do You Use a Personal Credit Card for Business Expenses? Read This Tax Court Case First.

A recent Tax Court case denied a $16,901 interest deduction because the business owners could not prove the debt belonged to the business or adequately document the underlying transactions. Learn how to avoid the same mistake.

Received an IRS Penalty Notice? What You Need to Know Before You Respond

Received an IRS penalty notice? Recent court decisions make some procedural challenges more difficult, but taxpayers still have powerful options for reducing or eliminating penalties. Learn which defenses work best and what to do before responding to the IRS.

Can The IRS Disallow A Tax Strategy That Follows The Tax Code?

A recent federal court decision denied more than $100 million of claimed tax benefits because the underlying transaction lacked economic substance. Learn what business owners should know before implementing sophisticated tax planning strategies.

A Missing Form 1099 Will Not Save You From The IRS

A recent Tax Court case confirms that receiving a Form 1099 after filing your tax return does not excuse unreported income. Learn how late tax documents can trigger IRS notices, penalties, and additional tax assessments.

The Overlooked Tax Free Employee Benefit: Educational Assistance Plans and Student Loan Repayment

Most employers have never heard of Educational Assistance Plans. Learn how your business can provide up to $5,250 annually in tax free education and student loan repayment benefits while receiving a tax deduction.

IRS Warns Side Hustle Owners: Hobby Income Is Still Taxable

The IRS recently reminded taxpayers that hobby income is taxable even when an activity is not operated as a business. Learn how hobby income is reported, why Forms 1099-K and 1099-DA matter, and how the IRS distinguishes a hobby from a business under IRC Section 183.

Employee vs. Independent Contractor: How to Avoid Costly Worker Classification Mistakes

Worker misclassification is one of the most expensive tax mistakes a business can make. Learn how the IRS determines whether a worker is an employee or independent contractor and how to avoid payroll tax penalties, audits, and compliance issues.

Mortgage Interest Deduction Rules: Lessons From a Recent Tax Court Case

A recent Tax Court case highlights the strict requirements for claiming the mortgage interest deduction. Learn when mortgage interest is deductible, why documentation matters, and how homeowners can avoid costly IRS challenges.

Cryptocurrency Staking Rewards Are Taxable Upon Receipt: What the Paschall Case Means for Investors

The Tax Court has now confirmed that cryptocurrency staking rewards are taxable income when received, not when sold. Learn how the Paschall case affects crypto investors, the IRS position on staking rewards, and what records you should maintain to avoid costly tax reporting mistakes.

How to Document Profit Motive for an IRS Hobby Loss Audit

Good records can be the difference between winning and losing an IRS hobby loss audit. Learn which documents impressed the Tax Court, how successful taxpayers proved profit motive, and the records every business owner should maintain under IRC Section 183.